Legal AI’s Ceiling is Jurisdictional: So Is The Opportunity

The bet is clear. The question almost nobody asks is: where in the world does it actually pay off?

Y Combinator’s recent Request for Startups names AI-native versions of professional services firms near the top of its list. Sequoia partners have argued for over a year that the first trillion-dollar company of the AI era will be a services firm, not a software company.

Law sits near the front of that conversation, and for good reason: the work is text-heavy, repetitive, regulated, and economically resistant to historical software - exactly why generative AI is now reshaping it.

The bet is clear. The question almost nobody asks is: where in the world does it actually pay off?

Law is not one market. It is roughly 200 - and the gap between them is the most underappreciated fact in the entire conversation about AI in legal services. This essay argues that legal AI is fragmenting along jurisdictional lines, not consolidating. The next decade of value will not be captured by a single global winner. It will be captured by a universal stack serving the world’s largest international firms - and by a distinct local champion in every jurisdiction large enough to support one. For founders, the question is not whether legal AI is a good market. It is whether the fragment they’re building for is large enough to support the company they want to build. The math is brutally honest, and most founders haven’t done it.

The Industry Built on Leverage

The business model that made BigLaw profitable is the one AI breaks first.

Law firms run on a pyramid: equity partners at the top, salaried associates in the middle, paralegals at the base. Associates at top US firms carry billable-hour targets of 1,700–2,300, which means 10–12 hour days to bill 7. On average, lawyers in private practice bill only about 37% of their working day. The economics worked through leverage - the spread between associate billing rates ($600–1,400/hour) and associate salaries ($225K–435K).

Document review in M&A diligence, litigation discovery, and regulatory matters was the engine of that spread: tedious, low-stakes, high-margin work, with burnout replacement costing $200–500K per associate.

When AI performs substantive associate work at production quality, it doesn’t just speed up the firm. It threatens the spread that makes the firm profitable.

What Legal AI Is Actually Doing

The popular reading - that AI accelerates document review - is years stale. The frontier is agentic, end-to-end, and increasingly absorbing legal labor rather than augmenting it.

Harvey reports more than 25,000 custom agents running M&A diligence, fund formation, contract drafting, and regulatory analysis end-to-end, some across workflows spanning weeks. Crosby, an AI-native law firm in San Francisco, runs simulations predicting how counterparties respond to redlines and voice agents that negotiate on a client’s behalf; its median contract turnaround is 58 minutes, and since exiting stealth in mid-2025 it has negotiated more than $1 billion in contracts. Enter, in São Paulo, processes more than 250,000 lawsuit defenses a year for enterprises including Itaú, Santander, Nubank, and Airbnb. What unites them is not the model but the scope: each runs the whole matter rather than serving as a tool the lawyer reaches for.

Then there is the platform layer. On April 30, 2026, Microsoft shipped Legal Agent inside Word as part of Copilot - clause-by-clause review, redlines in native tracked changes, deterministic edits - at $30 per user per month, the price most large firms already pay. Five weeks earlier Harvey had closed an $11B round with seats estimated at $1,200/month. The gap is roughly 40x. The commodity layer is here; what stays valuable above it is depth, workflow, jurisdiction, and liability.

That last word matters. The Damien Charlotin AI Hallucination Cases Database catalogued 1,348 documented hallucination incidents in court filings worldwide as of April 24, 2026. Sanctions have escalated from $500 fines in 2023 to a $110,000 penalty in Oregon and the first US indefinite license suspension tied to AI hallucinations, ordered by the Nebraska Supreme Court in April 2026; even Sullivan & Cromwell apologized to a federal bankruptcy judge that month.In every case, the lawyer who signed the brief carried Rule 11 liability - not the AI vendor.

The Unicorn Map, and the Story It Misses

Venture-scale outcomes cluster where two conditions meet - a large local legal market and English as the primary language. Where one is missing you find well-funded specialists; where both are absent, no unicorns. But the consolidation story San Francisco tells from that map misses what the world’s largest firms are actually doing.

Roughly nine pure legal AI unicorns exist as of May 2026: Harvey ($11B, San Francisco), Legora ($5.55B, Stockholm→New York), Ironclad ($3.2B), Relativity (~$3.6B), Clio (~$3B), EvenUp ($2B+), Justpoint (~$2B), Lawhive (~$1B+, London), and Enter ($1.2B, São Paulo). Just behind sits a well-funded cohort - Crosby, Eudia, Norm Law (San Francisco); Lexroom (Milan); Noxtua (Berlin); Law&Company / SuperLawyer (Seoul); LegalOn (Tokyo); Jhana (Bangalore).

Both conditions matter. Eight of nine unicorns are headquartered in English-speaking jurisdictions whose legal markets clear roughly $30B in annual spend. Where one condition is missing - Continental Europe has aggregate size but no shared language; most emerging markets have neither - you find specialists but no unicorns. The ninth, Enter, exists because Brazil’s 80 million active lawsuits, eight times the US figure, create a $50B+ market in a non-English jurisdiction. Legora makes the math visible: founded in Stockholm in 2023, it joined YC’s W24 batch and moved its HQ to New York. CEO Max Junestrand has been blunt about why - “It’s nine to one in terms of legal spending. It turns out the Americans love to sue each other much more than we like to do in Europe.” The US legal market is roughly $437B annually; Europe combined is roughly $50B.

That gap makes consolidation look inevitable from San Francisco. Harvey is in 60+ countries, Legora in 50+, and both have signed the world’s most prestigious firms; CMS rolled out Harvey to 7,000 lawyers across 50+ countries in December 2025. But the data underneath is more nuanced. Harvey’s own BigLaw Bench: Global benchmark, released February 2026, acknowledges that model performance degrades on jurisdiction-specific work - the benchmark exists because the gap is real, built with 24+ local legal experts.The expansion model looks less like software economics than services-heavy localization: Harvey plans to hire 180 people across Europe in 2026 and deploys embedded legal engineering teams inside customer organizations. CEO Winston Weinberg says the real pressure is not local rivals but foundation labs commoditizing the generic layer.

The single most telling data point: CMS - the firm that just rolled out Harvey to 7,000 lawyers - is also a co-developer and investor in Noxtua, the Berlin-based sovereign German legal AI. Dentons is in the same position; C.H. Beck, Germany’s dominant legal publisher, led Noxtua’s €80M Series B alongside both firms. The world’s largest firms are not standardizing on Harvey. They are hedging - Harvey for cross-border work, a local sovereign AI for in-country regulated work. Every major non-English market has now produced at least one well-funded local champion solving a structurally different problem: Noxtua (Berlin, ~€81M) builds sovereign German AI in German data centers, meeting the §203 StGB confidentiality bar that excludes US-hosted AI; Lexroom (Milan, $73M+) rebuilds its data infrastructure for each civil-law jurisdiction, its CEO framing the bet as “an AI legal engine that reasons data-first”; Enter sells outcome-based mass-litigation agents directly to enterprises; and Law&Company / SuperLawyer (Seoul, $36.3M Series C2) scored in the top 5% of the Korean Bar Exam and reached ~38% of Korea’s practicing lawyers within a year. Similar patterns are visible in Japan (LegalOn), India (Jhana), MENA (HAQQ, Qistas, Legora’s Arabic deployment with Al Tamimi), and emerging infrastructure in Turkey, CEE, and Latam. One thesis underneath: legal logic is jurisdictional, and sovereign data, codified law, local procedure, and non-Latin scripts are not problems Harvey solves at its unit economics.

Why Local Legal AI Is Durable

Local legal AI is not a temporary gap that closes as foundation models improve. Three independent forces hold it in place.

Sovereign data requirements - Germany’s §203 StGB, the EU’s GDPR, Turkey’s KVKK, China’s and Russia’s localization regimes - are regulatory walls, not preferences; Noxtua’s entire thesis rests on German firms being legally barred from using Harvey in certain workflows. Legal-system features unique to a country - Brazil’s 80M lawsuits, India’s 50M-case backlog, Mexico’s labor disputes, Turkey’s consumer and employment court load-create markets invisible from San Francisco; the winners don’t build “Harvey for [country],” they build products that only exist because the country exists. Language and codified-law non-translatability - civil-law reasoning is statute-first, common-law precedent-first; generic LLMs trained on English common-law text underperform on civil-law tasks, and the morphological complexity of Arabic, Korean, Turkish, Japanese, and Chinese widens the gap further.

The three drivers compound. Brazil has all three; Enter exists. Germany has the first and third; Noxtua exists. Korea has at least two; SuperLawyer is racing to capture all of it. Turkey has elements of all three - KVKK builds a GDPR-shaped sovereignty wall, consumer and employment court volume is high relative to GDP, and Turkish’s agglutinative structure plus specialized legal vocabulary create a strong language barrier that the HukukBERT research documented in detail in April 2026. The structural conditions for local legal AI exist. What they do not guarantee, on their own, is unicorn scale.

The Jurisdictional Ceiling, and Three Ways to Clear It

That the category is durable does not mean it produces unicorns everywhere. The math is brutal, and for founders in smaller jurisdictions only three paths reach venture scale.

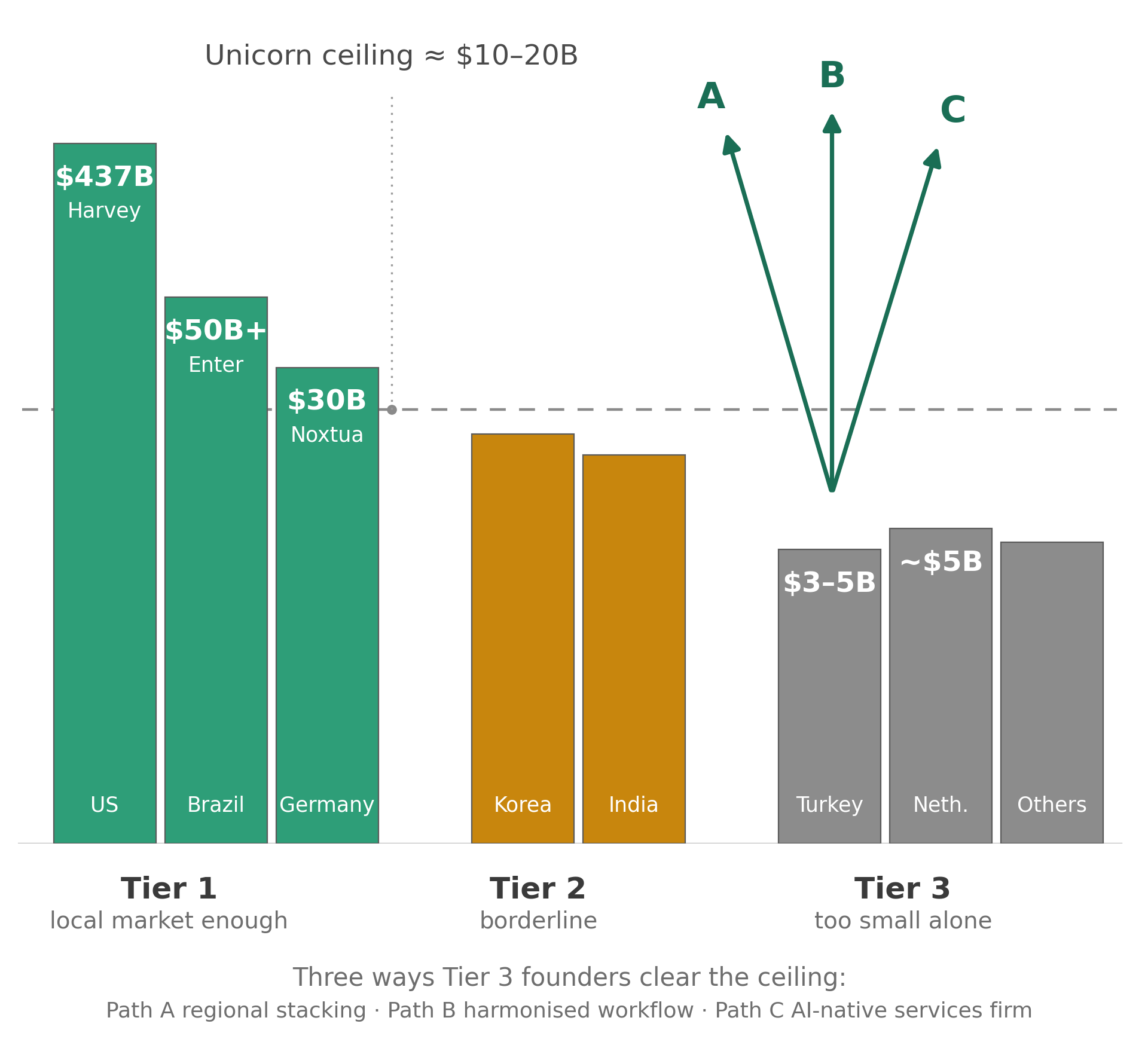

A jurisdiction-specific unicorn needs roughly $50–100M ARR at current 15-20x multiples - which requires an addressable legal-labor market of $10-20B annually, capturing 0.5-1%. That threshold sorts the world into three tiers. Tier 1, where the local market alone is enough: the US (~$437B), UK, China, Brazil, Germany, France, and Japan - Harvey, Enter, Noxtua, and LegalOn confirm it. Tier 2, borderline, needing a near-monopoly or adjacent expansion: Italy, Spain, Canada, Korea, Mexico, India - SuperLawyer’s 38% year-one Korean adoption is the only single-jurisdiction path that looks realistic. Tier 3, where a single-jurisdiction unicorn is structurally unavailable: Turkey (~$3–5B), the Netherlands (~$5B), and most of MENA, CEE, SE Asia, and Africa individually, where even a near-monopoly tops out around $150–250M ARR - real $300–500M outcomes, most likely via acquisition by Harvey, Legora, Thomson Reuters, or LexisNexis, but not unicorns.

Market size sorts legal AI into tiers. Only Tier 3 must clear the ceiling via a path — A, B, or C.

For Tier 3 founders chasing venture scale, three paths work.

Path A - Regional stacking. Build for a multi-country bloc that clears the ceiling in aggregate. Lexroom is doing this across civil-law Europe, Noxtua across DACH and Central Europe, HAQQ across pan-MENA. Hard to execute: the product must be jurisdiction-aware from the architecture up, and the legal systems must share enough structure to serve with one team.

Path B - Internationally-harmonized workflow. Pick work whose legal logic is international by construction - sanctions, cross-border IP, AML/KYC, trade compliance, international tax, ESG, IPO/SPAC. The TAM is global from day one. The trade-off: Harvey can reach these markets too, so the moat must come from depth, not geography.

Path C - AI-native services firm capturing local enterprise legal labor. The YC and Sequoia thesis recast for Tier 3 markets. The legal software market is small; the legal labor market - what enterprises spend on in-house counsel, dispute defense, regulatory and compliance - is materially larger. The structural reason it works: foundation models and software vendors can’t absorb Rule 11 liability; only companies structured as law firms can. Crosby, Enter, and Lawhive are the proof. Enter’s playbook - build an agent that takes the work, charge per outcome rather than per seat - produces a $300–500M outcome in Tier 3 today, not a unicorn, but the ceiling rises as enterprise legal volumes grow.

The Trillion-Dollar Law Firm

The first wave of legal AI made a small number of US companies very large. That wave is largely over. What comes next won’t look like Salesforce - one global winner per category - but like banking: a universal stack serving the world’s largest institutions, with local champions everywhere else, anchored in jurisdictions whose features they understand better than anyone in San Francisco ever will.

A trillion-dollar AI-native services firm is plausible. If one comes from law, it will come from a Tier 1 jurisdiction large enough to support the math, capturing legal labor spend rather than software seats, and structured as a firm that takes liability - the only structure foundation models cannot replicate. The defensible position is not the model and not the data; it is jurisdictional depth, owning a legal system the frontier can’t reach. Crosby is building that in US contract law, Enter in Brazilian mass litigation, Lawhive in UK consumer law. The pattern is small now; it will not stay small.

Legal AI is not a market. It is two hundred markets, each with a different ceiling, a different defensibility profile, and a different path to scale. The founders who understand which one they are in will build the companies that matter. The question is not whether legal AI is being rebuilt - that is settled - but which fragment you are building for, and whether it is large enough to support the company you set out to build. For most founders, that is the difference between a $300M outcome and a $3B one - worth answering before you start, not after.